How will be your life without television, air conditioner or laptop? Blank and boring, right? Gone are those days when these were considered as luxury items and their owners were given high regard in the society. Thanks to the changing times, these items now have become a necessity of today’s life. Right from enjoying the helicopter shot of M.S Dhoni on the ‘idiot’ box a.k.a television to baking cookies in a microwave, life without these ‘essential’man-made items is unimaginable.

So, what if these items face the brunt of Mother Nature? In the country, like India, where incidences of earthquakes, flood, cyclone, etc.; are not new, chances are high that these calamities disfigure the beauty of your house. And how can you forget the rising incidences of theft, burglary, or housebreaking cases, which still happen even if houses are installed with high-tech safety equipments?

Well, sometimes these events are beyond your control but what is within your reach is—insure the content of your house with a suitable content insurance policy.

If you are living in a building, your society or builder may have bought a structure insurance, if that is the case, you should insure the content of your house, which is equally susceptible to natural and man-made perils.

In the case of independent villas, you should buy a comprehensive home insurance policy to cover both the structure and content, however, if you are a tenant, you can buy a policy to cover content only.

What is content insurance?

As the term itself says, a content insurance policy covers only house content against various perils, like fire, earthquake, burglary, theft, etc. Usually, ‘content’ is defined as those items which you would likely to take with you at the time of relocation. Thus, content can include, jewellery, furniture, electronic items, clothes, etc. Some plans also cover fixtures, like curtains, carpet, etc.

What are the types of content insurance policy?

Mainly, there are two types of the policy:

- As New or New for old Policy= It says, that at the time of loss or damage, the insurer will settle the entire cost without deducting depreciation. However, if there is a theft, the insurer will pay the amount equivalent to the cost of the similar new content. Note, items covered under this section vary from one insurer to another.

- Indemnity Policy= The insurer settles the claim after factoring in depreciation, i.e., wear and tear. Like, in case of damages caused to a four-year LED, the insurer will settle the claim based on the current value of the electronic and not on the basis of its market price. If you work from home, check whether your content insurance covers for business equipments or not.

What is the right coverage?

To arrive at the right content sum insured, check your insurer’s definition of valuables which can vary widely. Then you need to find the ‘article limit’, which is the maximum amount that an insurer will pay at the time of claim. It means, if you have jewellery or an item above that limit, it is necessary to inform the insurer about it and, probably, you would have to pay an extra premium to get it covered. After reading this, if you think you should hide the real value of items to save your money, then you should understand that in the case of loss, you would be alone to bear the burden. So, it is imperative to disclose the correct value of all the items which you want to bring under your content insurance umbrella. While, some insurers insist on photographs of the items as an authentic proof of their existence, many insurance companies don’t go into detail and rely on the list submitted by an insurance applicant. In the case of high-value items, valuation certificates from jewelers may also be required. Note, in any case, cash is not covered.

Remember, jewellery and artifacts can be covered in a separate insurance policy with extra premium. While, the age of content, like furniture, utensils, etc.; should be less than ten years, portable equipments like tablets, mobiles, laptops, etc.; are covered only if they are not more than five years old. However, the price of the total insured content should not be less than 10% of the value of the house. As stated above, those staying on rent, can only insure their content and valuables, and don’t require to take insurance for the structure ofa flat.

What happens at the time of claim if you have a partial cover?

Though, it is necessary to buy a comprehensive content insurance policy, it is equally important to buy a sufficient cover, otherwise, it will be equal to no coverage. An insufficient cover leads to underinsurance and low claim amount. For instance, if you buy a cover of Rs 5 lakhs for furniture worth Rs 10 lakhs, the insurer will pay only Rs 5 lakhs at the time of loss even if there is a total damage. In such a case, the insured (i.e., you) shall bear the remaining losses or damages.

What happens to your claim if at the time of loss your house was unoccupied?

Any loss or damage will not be settled if the loss occurred when a house was unoccupied. The insurer doesn’t cover losses from burglary or theft if your house remains unoccupied for more than 30 days without prior intimation to the insurer.

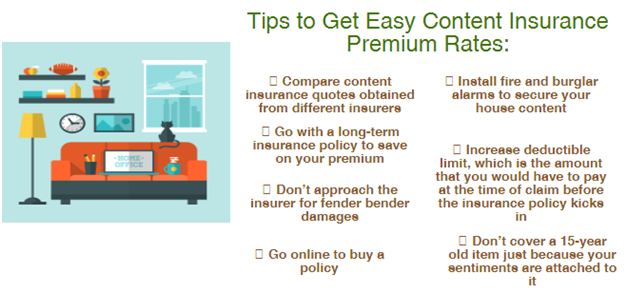

How is premium computed?

The premium varies according to the sum insured. It means, if you go with a Rs 10 lakh content cover, out of which Rs 2.50 lakh is the value of the jewellery, you would have to pay Rs 9,430/- yearly. However, if you trim the cover to Rs 5 lakh, out of which the value of the jewellery is Rs 1.25 lakh, the premium cost comes down to Rs 4,716 per annum.

As a home insurance policy is a bouquet of various covers, like jewellery insurance, personal accident cover, burglary insurance, etc.; some insurers also give discounts if you opt for more than four insurance sections.

How to file a claim?

Every insurance company has a toll-free number or an SMS alert code which you can use to contact the insurer and register your claim. Once the claim is registered, you need to duly fill the insurance claim form, with complete details of the loss and valuation of items. A FIR or police report in case of theft or burglary and a detailed report from the fire department in case of fire is needed. Also, don’t tamper with damaged items until the claim has been surveyed by the insurer’s surveyor as the claim will be settled only when the insurable interest is identified and losses are assessed.

In the case of losses or damages due to natural calamities, insurers usually relax the claim settlement process and documentation criteria.

What should you do at the time of policy renewal?

At the time of policy renewal, revisit your insurance policy to ensure it is in sync with the current scenario. So, if for example, in a previous year, you dumped high-end items, like electronics, antiques or jewellery, etc.; inform the insurer about this and get your insurance cover recalculated accordingly. Similarly, at the time of policy renewal, update your jewellery cover as per the current price of silver and gold.

Likewise, if you’ve made a series of purchases, inform the insurer if you want them to be covered under your policy. For instance, if you have replaced the entire furniture of your home, then you might need to increase the sum insured accordingly and for that, intimation to the insureris required.

Remember, though, buying a content insurance policy is not a necessity, it is vital to save yourself from unexpected loss. As it is said, “Precaution is always better than cure,” so go with a content insurance to keep the beauty of your valuable items intact.

Author Bio-